Is Polymarket Exploitative?

No, even if you should be careful betting on people

Nobody objects to weather forecasts. If we bet on whether it would rain tomorrow, nobody would have a worthwhile complaint. Of course, you’d have people who object to bets on principle, but we aren’t worried about them. Life is a series of implicit bets and they might as well tell us that they want to ban borrowing to go to college or to buy a house. For most of us, this much is clear: the weather can sustain an unobjectionable prediction market.1

Okay, you might say, that’s my intuition about rain—what about hurricanes or flash floods or a volcanic eruption? Isn’t there something icky about betting on events that will kill people if they happen? For precision, let’s call these causally impotent lethal markets.

The obvious problem with this ick response is that your disgust is minimally important compared to the epistemic benefits conferred by the prediction market. Having an accurate probability of a terrible thing happening helps everyone potentially affected by the terrible thing to plan accordingly. It helps to weigh Terrible 1 against Terrible 2, it helps to figure out the expected scale, and even what the aftermath might look like.

Maybe you’re of the view that meteorologists are better than prediction markets at assigning accurate probabilities to these sorts of things. That seems unlikely. Nevertheless, you have to grant that we do not have the equivalent of meteorologists in all of the spaces where it would be (life-savingly) useful to provide people with probabilities of things happening.

For an example that should hit close to home for anybody and everybody: pandemics! If you’re anything like me, then it’s likely you’re underestimating the probability of bird flu (H5N1) breaking out into the next global pandemic. That’s useful to know. Now, conditional on a human-to-human bird flu outbreak, there are still lots of questions about its scale and lethality that need to be answered before you can map out contingencies. Fortunately, there are no in-principle reasons not to setup (higher uncertainty) markets for that too.

An important fact about these markets is that the way they go is not obviously tied up in the behaviour of one or a small handful of individual actors. That’s where the causal impotence is coming from. If someone places a $500k bet on a hurricane developing over the Gulf of Mexico (America?), then there’s no reason to suspect they are working to bring about a hurricane, since a hurricane is not the sort of thing you can work to bring about.2

I focus on causal influence because I think it’s what gives people the ick about insider trading. There might be a fairness complaint about people betting based on inside information—see this Google ‘Year in Search’ story and this one about the Maduro raid—but neither of these people were causal influences on the result of the market (unless Trump or Rubio really needed $400k). A Google employee cannot alter what the world searched for, but they can see the data before it goes public; likewise with a U.S. officer. That means they benefitted by providing true price signals to everyone else in the market. What’s exploitative about that?

Consider, on the other hand, Jontay Porter.

In high school, Jontay helped lead his high school to a perfect season alongside his older brother,3 taking the Washington state championship and winning him scholarship offers to a number of top basketball schools. Then, he grew two inches, catapulting him into ★★★★★ territory. His father became a coach at Mizzou and Jontay committed to go play under him with his brother, keeping the storybook arc going.

At Mizzou he didn’t disappoint. After a slow start, he played well-enough to be ranked among the likes of now-MVP Shai Gilgeous-Alexander as one of the eight best freshmen in the SEC. He had to—his brother Michael, a top two prospect in the nation, went down with a season-ending injury in the first half of the season opener. Despite the bad brute luck, Mizzou went on to make the NCAA tournament, giving them a shot at a national championship.

Facing down Florida State, Jontay shot a meagre 14% in a brutal blowout loss. Afterward, he tentatively declared for the NBA draft alongside his brother, expecting to be a late first round pick. But something gnawed at him—a job unfinished. On the day of the deadline, he withdrew his name, returning for another season to Missouri.

And then disaster struck. In a preseason scrimmage with the team, he tore both the ACL and MCL in his right knee, ending his year and tanking his stock in the draft. Then he tore his ACL again. It was too much risk for NBA teams to stomach. Despite declaring for the next draft, Jontay went unchosen, signing with the Grizzlies without much in the way of hope.

Perhaps the stunning fall from grace is what led him to place “an $80,000 same-game parlay bet” that he would underperform on multiple stats that, if it hit, “would win $1.1 million.” He then checked into the game for three minutes before suddenly falling ill and exiting for the rest of the night.

Jontay’s bookie did not pay out the winnings, so the bet’s lasting legacy is as a textbook example of causal potence in a prediction market. In a market about what Jontay does, Jontay is the master manipulator.

So maybe prediction markets are exploitative when master manipulators waltz into an otherwise healthy market and decide to profit off everyone’s epistemic labour by betting on the most profitable thing they can do, and then they go and do that thing.

More examples: Starmer betting on his own resignation, Musk betting on how many tweets he puts out, Trump betting on pardoning Ghislaine Maxwell, and so on and so on—these all represent opportunities for master manipulators to go to work exploiting people in prediction markets.

But what element of the betting can we point to as the part where exploitation enters in? We’ve dismissed the epistemic fact of having inside information. It’s not exploitative to reap a reward for your information, or else everyone with edge in a market would be exploiting everyone else. Is it just the causal fact of being a master manipulator?

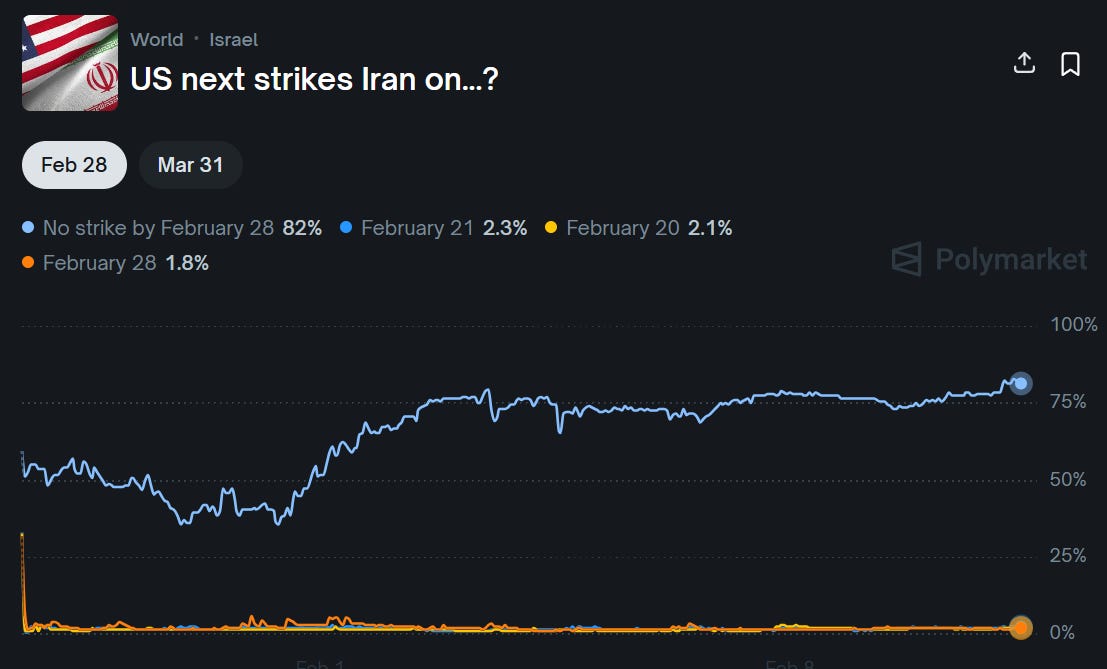

We might benefit by zeroing in on the people being exploited. Let’s take the most morally-charged prediction spaces: causally potent lethal markets. Suppose Trump, in relatively direct control of U.S. military capabilities, bets NO on ‘No strike by Feb 28’ in the US next strikes Iran market. He then directs his generals to hit Tehran, killing a mix of IRGC forces, regime non-combatants, and civilians. As a result, he makes a huge profit.

The most obviously exploited people in this case are the deceased Iranians, because in this story they have had their lives ended involuntarily—primarily as a means for personal profit. That’s messed up. Everyone has powerful legitimate reasons not to want other people to treat them this way. If exploitation exists (it’s famously hard to define), then this seems a textbook case.

So at last we have a principle:

(Market-Driven Evil) If a Master Manipulator trades in a market in order to align their incentives with directly harming people, then there is exploitation in that market.

But Jontay did not violate this principle. Direct financial harm resulting from a prediction market is a bit of a slippery concept, but it is safe to say that nobody’s livelihood was tied up in which way his bets went. They aligned his incentives to shoot a basketball badly, not to go and kill people.

Going back to Trump and Iran, in what sense are the other bettors in the market being exploited? After all, it would be wrong to bomb anybody for the sole purpose of profiting, so pointing that out doesn’t tell us anything interesting about prediction markets. The fact it operates through perverse incentives is good to know, but it’s equivalent to the obvious wrong of purposefully cultivating a disposition to harm people.4

(Market-Driven Exploitation) If a Master Manipulator trades in a market in order to align their incentives with increasing the number of losers in that market, then there is exploitation in that market.

Now, everyone trading in a market wants to win. In a technical sense, Polymarket is zero-sum, in that every dollar won in a market is a dollar lost by someone else. So win-seeking is loss-maximizing for others, regardless of who you are. What the principle says is that if you are specifically a Master Manipulator, win-seeking is exploitative (and thereby wrong).

But why? It seems hard to explain without appealing to it being unfair for other bettors—but the unfairness of prediction markets isn’t our question.5

Return to Trump and Iran one more time, but imagine now that Trump was already going to strike Iran and is simply raking in profit over it without altering his own incentives. This requires a little bit of imagination, because it could be that he made the decision and had some time to reverse course, so that now by betting he is altering the incentives around changing his mind. For that reason, you should think of the case as one where the operation has quietly begun and Trump cannot really stop it. In this case, there’s no incentive alignment—it’s just like the case of the Google trader, where an outcome was going to happen and an insider bet helps to better align the public’s probability towards 1. Really, just looking at the facts of the case, Trump is just acting as another bettor, not a Master Manipulator.

Still, there’s an intuitive ick here. I suspect that comes from the sense that Trump is behaving like a parasite on the market. Everyone else in it had to do epistemic labour—they thought things over, weighed the contingencies, and assumed risk—and here comes Trump needing to do none of that because he’s the boss and already gave the order. One party is playing a risk game and one is enjoying a free lunch.

If the ick is well-placed, it looks like the exploitation of other bettors comes from free-riding off of them for that free lunch. Unfortunately for the view, it clashes with the more rational read, which is that everyone in the market has benefitted by the provision of true price signals to everybody in the market. Trump isn’t free-riding, he’s bringing useful information to the table. It’s on the other bettors to discern that, like they would need to with any bettor showing up with an edge.

We’re still left with the suggestion that what morally matters might be Master Manipulators changing what they were going to do because of the existence of the prediction market. These markets offer huge financial incentives to enter and profit off of one’s position, turning potential manipulators into actuals. But framing this as exploitative of anybody else is a difficult sell.

If anything, it suggests prediction markets might be corrupting, creating incentives that lead to harming not other bettors, but the public interest. This is a more legitimate concern, even if there are good replies available, many of them rooted in institutional design. Look at what happened to Jontay—he got banned from the NBA forever. He used his edge for corrupt free-riding and the system was designed to make sure his edge was taken away as a result.

Taking the corruption objection seriously also requires recognizing that there are solutions; no need to throw away enormous epistemic benefits in order to avoid a few players making ugly plays.

Just make it hard to play ugly!

More generally, day-to-day weather is part of a class of causally impotent non-lethal markets. The stakes aren’t obviously moral and buyers and sellers aren’t outcome-determinative. These also, popularly, include markets on the Federal Reserve’s next moves, the next jobs report, the next CPI number, federal elections, etc.

Technology might be progressing to the point where pandemic-level hazards are the sort of thing you can work to bring about.

NBA Champion and 25ppg scorer Michael Porter Jr.

If I have good evidence a book titled ‘Why You Should Eat People’ is persuasive and I choose to read it credulously, and this leads me to become the sort of person who eats people, then I’ve acted wrongly in choosing to read the book (in addition to whatever people-eatings I end up engaging in).

There’s a few reasons why it, ostensibly, seems misguided to worry about fairness in prediction markets. To reiterate the core of an article I wrote about a year ago, the purpose of these markets is to provide the public good of accurate probabilities of future events, not to make sure the deserving are turning a profit. That’s not to say there aren’t interesting questions to raise in this space, but the naive fairness objection to such markets is more psychologically compelling than it is normatively.

I already agreed before reading but enjoyed walking through and imagining the counter arguments nonetheless !