Give Us Prediction Markets

An epistemic super serum

Wouldn’t it be nice if you could work with decently accurate probabilities of future events? Prediction markets allow this to happen, setting up exchanges for contracts that payout to traders based on the outcome of an event they’ve predicted.

Nobel economist Kenneth Arrow endorsed them for some very simple reasons, and you should too:

Information is widely dispersed in society, and it is highly desirable to find a mechanism to collect and aggregate that information. These markets work for several reasons: First, almost anyone can participate. Second, people think hard when they have to back up their predictions with money; buy the right presidential contract and you win, buy the wrong one and you lose. Third, the profit motive encourages people to look for better information.

They’re pretty awesome! Here are some current market results pertinent to our recent posts:

The Metaculus community gives China a 34% chance of controlling half of Taiwan by 2050.

Polymarket gives Mark Carney, ex-central banker, a 81% chance of replacing Trudeau as PM and getting to face Poilievre in the next election.

Climate Change Can’t Wrong Future People

Metaculus estimates global warming to come in at 3°C by 2100, with 95% agreeing it will exceed 2°C by then.

Sports Betting: Experiment Gone Wrong

The most popular form of direct prediction market is the sportsbook, and for various reasons, their proliferation has been controversial.

Last year, Americans wagered something like $130 billion on sports, a completely degenerate amount that should only be expected to rise in the coming years. The tsunami began in 2018 when SCOTUS scrapped a federal ban, and betting is now a ubiquitous part of every North American sports broadcast. This has—understandably I think—struck a nerve with fans, who regardless of their personal stance on the matter, tend to resent its crowding out of commentary on the actual athletes and games.

Lots of thinkpieces and profiles have been written criticizing sports betting: in The Atlantic, The New Yorker, and the NYT/Athletic. There’s also been a number of incisive pieces here on Substack: from Brian Moritz, Zvi Mowshowitz, and a look into the practice in Africa by Reuben Mwatosya.

What sticks out is that there’s little effort to attack the practice of gambling on the prediction of sporting outcomes. Instead, issues of predation dominate the discussion, focusing on how apps are designed to exploit addictive tendencies built into our psychology, the inescapability of betting itself for any fan of the game, and the permanent accessibility of mobile devices.

That is to say, the discourse has turned against sports betting because it has designed itself, as an industry, to be there, waiting, for the slightest of urges, to which it can present itself as instant gratification. There is nothing sober about this process—they shower you in bonus bets, encourage you to parlay several winnable wagers into moonshots, and chase you algorithmically wherever ads are served until you give them a try.

Mowshowitz makes this point vivid:

For [addictive gamblers], this is like an alcoholic being forced to carry a flask around in their pocket 24/7, while talk of what alcohol to choose and how good it would be to use that flask right now gets constantly woven into all their entertainment, and they by default get notifications asking if now is a good time for a beer. You can have the apps back up and running within a minute, even if you delete them.

But again, it’s not the principle of betting on outcomes that public opinion is rallying against. I am skeptical that there would be anything resembling this sort of backlash to betting infrastructure if it looked less like a casino and more like retail trading at Schwab. While the sins of FanDuel and DraftKings ought not to be repeated, they aren’t reasons to oppose prediction markets with more appropriate rules.

Election Betting: Experiment Gone Right

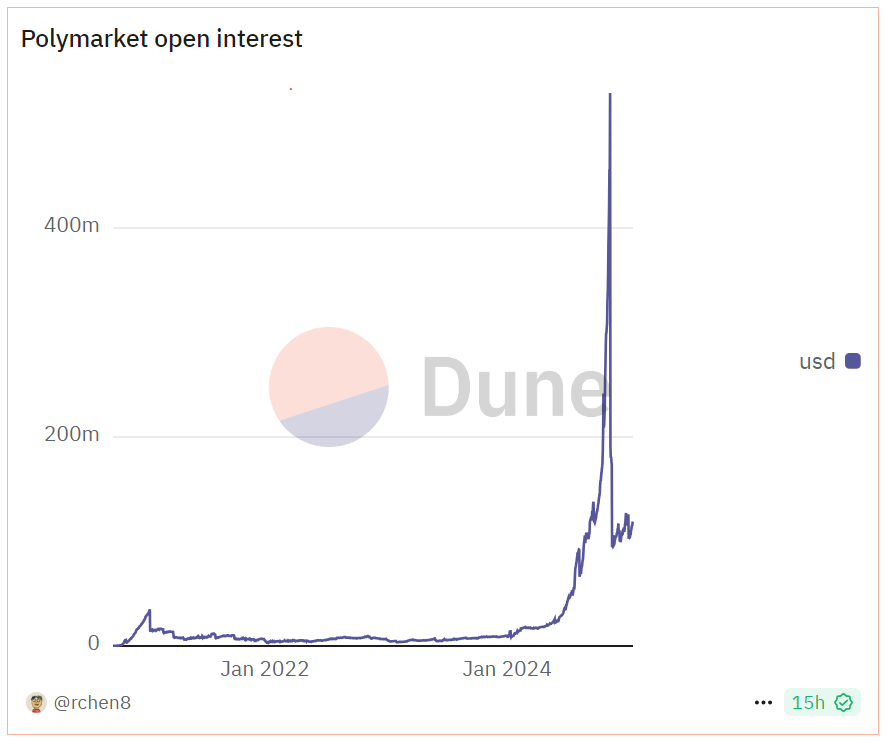

2024’s big success in this field was the presidential election, where traders bet $4 billion on who would win—the biggest election market ever. Sites that takes wagers on politics and other current events are more explicit than sportsbooks about presenting as what they are: prediction markets. Polymarket—ran on cryptocurrency—is the most popular, handling $9 billion in volume across all predictions in 2024. Some of its brethren include Manifold, which operates using play-money, Metaculus, where traders stake reputation, and Kalshi, the first federally regulated real-money player in the field.

These markets, which gave Trump a slight edge over traditional polling averages and popular forecasters, enjoyed an incredible surge in usage over the course of the cycle. Now, they’ll be legally available on various other popular platforms, including IKBR, Crypto.com, and Robinhood.

And they’re really good at predicting these things. In the linked chapter available from Brookings, the authors find that when prediction markets are setup around clearly defined questions that the public is interested in, their prices tend to outperform opinion polls.

There are some questions of this sort that will still fail. The authors discuss Supreme Court nominees predictions failing because there is no widely dispersed information about the question—only those inside the White House making the decision have anything interesting to signal, and their lips are sealed.

Most elections are well-suited to markets however, with each bettor able to bring their own knowledge to piece together with that of their social circle and the broader world. When hundreds or thousands of people bet this way, the market price captures and aggregates all of this scatted information. The numbers back this up clearly. When researchers compare market predictions to opinion polls before elections, the markets consistently show smaller errors. This holds true both right before elections and months in advance.

Besides the predictive signals they generate, these political markets avoid the aforementioned sins of sports betting. There aren’t the annoying ads, predatory apps, or outrageous introductory offers designed to entangle unsuspecting newcomers… at least not yet.

Because the United States’ CFTC has been inexcusably slow letting services like Polymarket break into the market, a serious conversation about how to regulate these platforms has not taken place in the public square. That should change.

What Should the Rules Be?

Aren’t prediction markets legal abroad? Why don’t more people use them? Why is Kalshi allowed to run while Polymarket isn’t?

Questions abound; last year, Nick Whitaker and J. Zachary Mazlish took a stab at explaining why we don’t see many of these markets. It’s probably the best piece on this subject and I would highly recommend it. Very roughly, here is their argument:

Savers aren’t interested in predicting, since it’s a zero (or negative) sum game.

Gamblers aren’t interested in waiting, often until the end of the year, for predictions to resolve.

Sharp analysts don’t expect to profit without these groups’ money in-play. Ergo, the market lacks liquidity and what profits do exist are necessarily small.

Presidential elections excite gamblers and hence attract some sharps, but are uniquely anticipated events that can’t be replicated.

Taken as a whole, their article explains why free markets probably won’t lead to the proliferation of prediction markets. This helps explain why they aren’t common outside the United States, where in many cases they are perfectly legal to operate and participate in.

But accurate probabilities of future events are a public good, and their epistemic value gives government a case for subsidizing their production. They could do this by acting as a market maker, guaranteeing traders the ability to buy and sell contracts on important questions.

Whitaker and Mazlish are bearish on the idea of subsidies, in part because of research indicating small teams of ‘superforecasters’ can and do perform equally as well as existing prediction markets. On their view, much of what would be achieved is already available to major institutions, who employ consultants, spies, economists, and data scientists to model the future.

A sufficiently liquid exchange would make this modelling publicly-available, with continuous live updates as new information becomes available, and provide a valuable standard against which to evaluate the unexpectedness of powerful people’s decisions.

Since the goal in the end is prediction accuracy, regulators should not worry about insider trading, which incentivizes those with important private knowledge to help calibrate better probabilities by rewarding them with profit.

Part of why Kalshi is allowed to operate in the United States and Polymarket isn’t comes down to the CFTC mandating rules that harm prediction accuracy, including:

Monitoring the use of material nonpublic information.

Restricting which topics can be traded in the name of the public interest against morally offensive markets.

Limiting trades on a given event to $25k.

Shutting out, for the moment, non-US traders and liquidity.

None of these are obviously justified, and it shouldn’t be shocking that a site like Polymarket has avoided coming into compliance with the CFTC’s rules. Given Donald Trump Jr. has just been hired by Kalshi, it remains to be seen whether the new administration will loosen the rules for all prediction markets, or push to shut the door on further competition in the space. For what it’s worth, the new CFTC chair seems at least somewhat friendly to the concept.

In Closing

Sports betting has caused a lot of problems and preys on psychological weakness to perpetuate itself. That is not what’s being advocated here. Think about how hard it is to get a clear, concentrated picture of the future—experts disagree, polls are snapshots, and everyone has their own opinion based on limited information. But when people can bet real money on their beliefs, all of those scattered pieces of knowledge come together to get us much closer to the truth. Hell, they do a great job when they’re just putting reputation on the line.

We should whittle down the regulations on prediction markets to focus on fraud prevention and strongly consider, as a society, subsidizing liquid markets on questions of public interest. This would be a small step towards improving everyone’s internal model of the world.